Chainrisk Simulation Engine

Chainrisk Simulation Engine provides rapid, precise DeFi risk assessments using Rust-based simulations & on-chain data, optimizing protocols for resilience & cost-efficiency.

November 8, 2024

ChainRisk deep dived into a recent research paper published on the economic risks of Renzo Protocol. This blog is to highlight major inferences & conclusions from the actual research paper.

The total value locked (TVL) in EigenLayer has grown rapidly to approximately $19.5 billion; however, the total value redeemable (TVR) is only about two-thirds of the reported TVL, highlighting potential vulnerabilities & risks. Renzo's protocol allows for leveraged restaking of liquid staking tokens, more than doubling returns compared to leveraged staking alone, but loans collateralized by Renzo’s liquid restaking token (ezETH) are susceptible to liquidation if ezETH depegs.

Given that the majority of staking is on Ethereum, any stress events from depegs could disrupt all protocols involved with staking & restaking on Ethereum & EigenLayer, spreading credit contagion throughout the DeFi ecosystem & potentially leading to another DeFi winter. This report has been heavily inspired & adapted from C. Alexander’s recent paper “Leveraged Restaking of Leveraged Staking: What are the Risks?”

In PoS blockchains, participants can stake their native tokens to run validator nodes, which propose & attest to the next block in the blockchain. In return, they earn rewards consisting of newly minted tokens & transaction fees. Tokens staked directly on the network are locked & cannot be traded or used as collateral.

Liquid staking protocols provide a solution to the locked token problem. When a staker deposits native tokens into a liquid staking protocol, they receive a fungible liquid staking token (LST) in return. LSTs can be used for trading or as collateral in other decentralized finance (DeFi) protocols, making staking more flexible & capital-efficient. By depositing ETH in Lido, stakers receive stETH tokens, which can be used as collateral or for trading while still earning staking rewards.

.png)

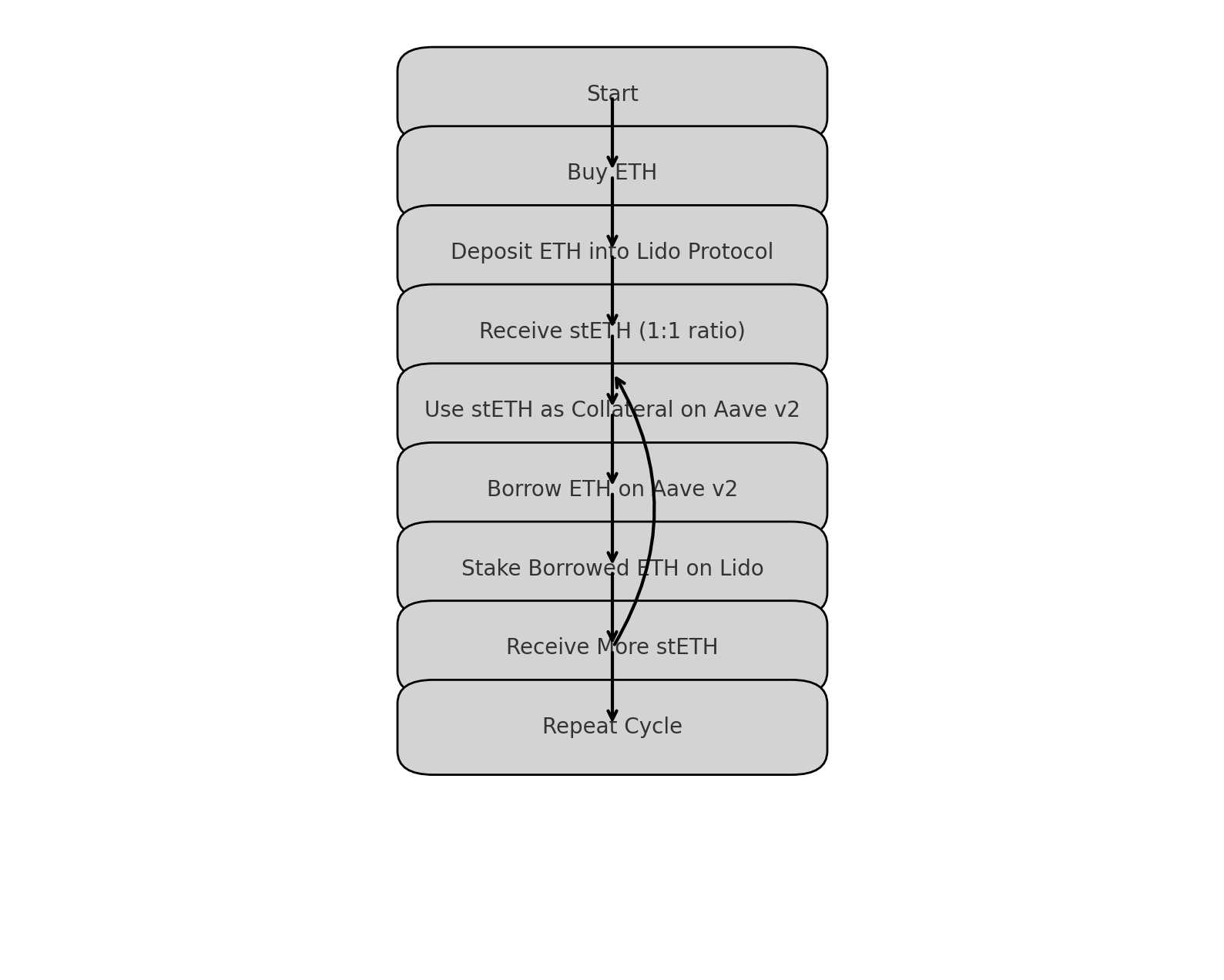

stETH is a rebasable token, meaning its quantity in the staker’s wallet increases daily to reflect accrued rewards, which can complicate its use in some DeFi protocols. Leveraged staking involves using LSTs as collateral to borrow more native tokens, which are then staked again to receive more LSTs. This process, known as looping or folding, can be repeated multiple times to amplify staking rewards. A common strategy involves using Lido’s stETH as collateral on Aave to borrow more ETH, which is then staked again via Lido, leveraging the initial investment multiple times.

Restaking is a recent development where tokens are staked on platforms like EigenLayer instead of directly on Ethereum. These platforms allow staking to support various actively validated services (AVS) within the Ethereum ecosystem. Restaking can offer higher rewards due to additional slashing risks associated with validating these services. EigenLayer, for example, imposes higher slashing penalties to compensate for the increased risk, but this also means that restakers need to carefully manage these risks.

TVL measures the value of assets managed by a DeFi platform. However, this can be double-counted in liquid staking & restaking processes, where the same assets are counted multiple times across different protocols. Renzo Protocol is a major liquid restaking protocol, contributing to EigenLayer’s TVL. In the upcoming discussion, we will discuss the double-counting issue, where the same ETH can be counted as TVL on multiple platforms. LSTs & restaking tokens can depeg from their native token prices due to various factors, including market manipulation & low liquidity in decentralized exchanges (DEXs). Depegging can trigger liquidation cascades, where collateralized loans become undercollateralized, leading to forced liquidations & further price drops. This could lead to widespread credit risks & potential contagion across the DeFi ecosystem, affecting multiple protocols.

Leveraged liquid staking involves using liquid staking tokens (LSTs) as collateral to borrow more of the native token (e.g., ETH), which is then staked again to receive additional LSTs. This process can be repeated multiple times to amplify the returns from staking rewards.

This loop can be repeated several times to leverage the initial ETH deposit many times over. Leveraged liquid staking can significantly increase staking rewards by repeatedly using stETH as collateral to borrow & stake more ETH. Increased leverage comes with higher risks, particularly the risk of liquidation if the price of stETH depegs from ETH. The total value locked (TVL) in DeFi protocols can be overestimated due to the recursive nature of leveraged staking.

Total Staked Value Calculation

Points to be Noted

This Table reports 20 rounds of leveraged staking using an initial capital of 100 ETH, each round having an LTV of 70% when the stETH price is 0.99

Observation:

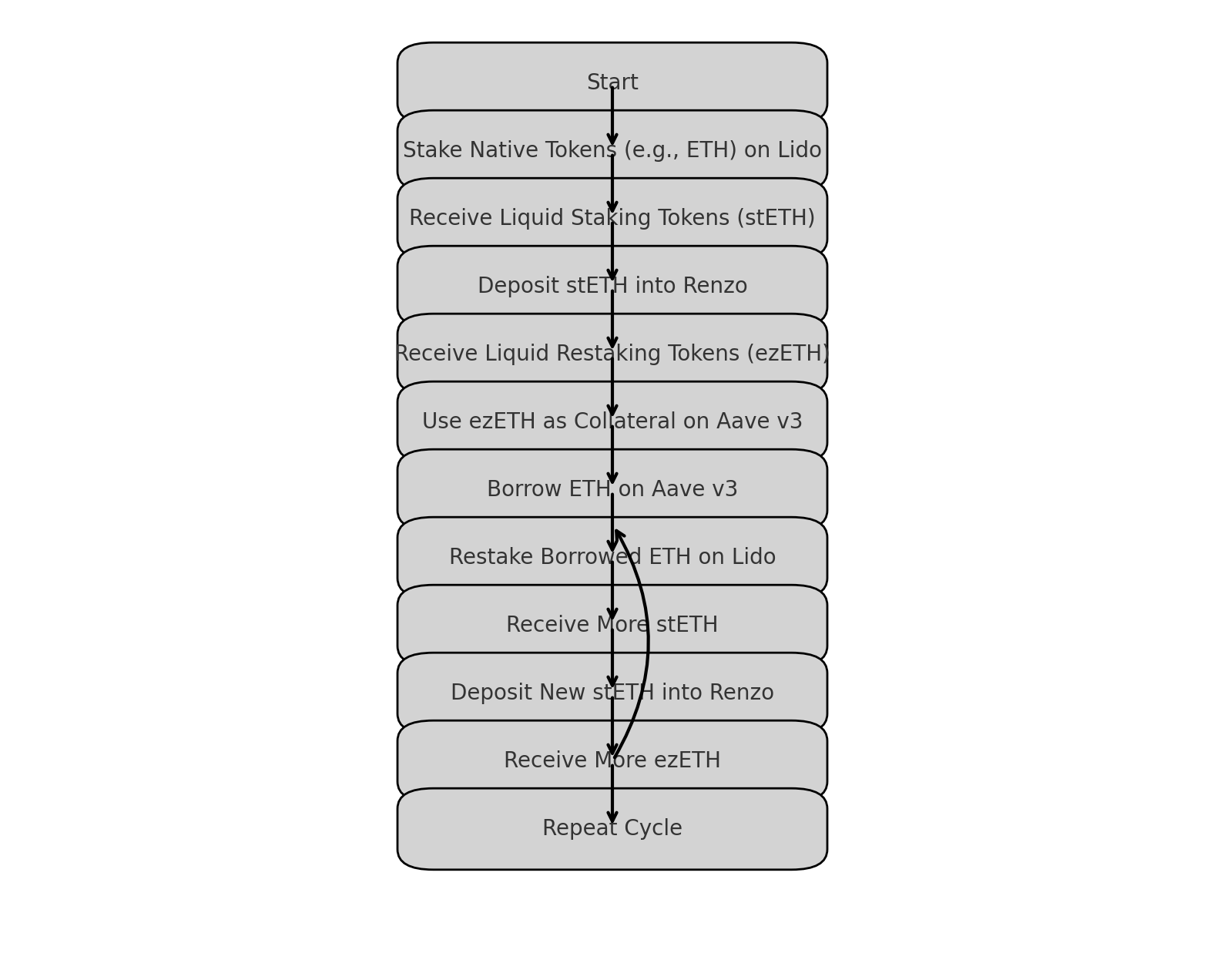

Leveraged restaking is a strategy that builds on leveraged staking by adding an additional layer of complexity & potential returns. This strategy involves staking assets on a Proof-of-Stake (PoS) blockchain through a liquid staking protocol, such as Lido on Ethereum, to receive liquid staking tokens (LSTs). These LSTs can then be used as collateral to borrow more native tokens (e.g., ETH), which are restaked to receive more LSTs, & this process is repeated multiple times to leverage the staking position.

Leveraged restaking can significantly amplify the returns from staking by generating multiple streams of income from both the staking & restaking rewards.

TVL Considerations

The TVL table explains how the reported TVL values can be misleading due to leveraged staking & restaking activities.

They do not reflect the actual amount of new ETH deposited but rather the repeated use of the same ETH as collateral.

Observations on EigenLayer TVL:

In lending protocols like Aave, the health factor & liquidation thresholds are crucial metrics for managing the risk of liquidations.

Health Factor= (Collateral Value×Liquidation Threshold)/Borrowed Value

A health factor greater than 1 indicates a safe position, while a health factor below 1 indicates that the position is at risk of liquidation.

A depeg event occurs when the price of an LST deviates significantly from its peg (usually the native token it represents). For instance, if stETH (a liquid staking token for ETH) depegs from ETH, the value of the stETH collateral drops, increasing the LTV & reducing the health factor.

When a borrower initially borrows ETH using stETH as collateral, the LTV is based on the current price of stETH relative to ETH. If stETH is worth 0.99 ETH, & the target LTV is 70%, the borrower can take a loan up to 70% of the value of their stETH collateral.

Suppose the price of stETH falls to 0.90 ETH. The value of the collateral drops, increasing the actual LTV. If the actual LTV exceeds the liquidation threshold, the health factor drops below 1, & the loan becomes eligible for liquidation.

When the health factor falls below 1, liquidators can step in to repay part of the debt & acquire the collateral at a discount. This creates a cascading effect:

This risk of cascading liquidations due to depegs highlights the systemic vulnerabilities in leveraged staking strategies. Professional liquidators can exacerbate this risk by targeting positions close to liquidation thresholds, leading to significant market instability.

Renzo Protocol is a liquid restaking platform that allows users to restake their liquid staking tokens (LSTs) on EigenLayer. In return, users receive ezETH, a liquid restaking token. Renzo Protocol aims to enhance the returns from staking by leveraging the staking rewards from both Ethereum & EigenLayer.

Key risks associated with Renzo’s Liquid Restaking Token (ezETH) include:

There are several historical incidents where depegging of liquid staking tokens (LSTs) led to significant liquidations & broader market instability. Key examples include:

Depegging often leads to significant outflows from liquidity pools, exacerbating price declines & increasing the likelihood of further depegs. For example, if large amounts of stETH are dumped into a low-liquidity pool, it can drive the price down further, triggering more liquidations. DeFi protocols are highly interconnected, with many protocols relying on the same collateral types & liquidity pools. A depeg in one protocol can quickly affect others, as collateral values drop & health factors fall below safe thresholds.

Liquidators play a crucial role in this dynamic, as they are incentivized to identify & liquidate vulnerable positions. This can create a feedback loop, where initial liquidations lead to more depegs & further liquidations. A depeg in ezETH can have broader implications for the DeFi ecosystem. As leveraged restaking positions are liquidated, other collateral types & interconnected protocols can be affected, leading to a wider contagion effect.

There are a couple of proposed approaches by the author of the paper itself such as developing optimization functions for optimal risk hedging between LSTs & LRTs & solving them. We could also use some particle filter methods like Monte Carlo & so on to simulate the depeg events & create the optimal parameters for AAVE & Renzo Protocol simultaneously to maintain a healthy coupled peg range using the ChainRisk Risk Platform itself. The area is ripe with research directions & there is ample space to innovate.

Leveraged staking & restaking can significantly amplify returns but also introduce substantial risks. Depeg risks & liquidation thresholds are critical factors that can trigger liquidation cascades & credit contagion. Detailed mathematical analysis & simulations can help quantify these risks, providing valuable insights for risk management. By using these detailed analyses, Chainrisk can demonstrate its capability to identify & mitigate economic risks associated with DeFi protocols like Renzo Protocol. The simulations & tools offered by Chainrisk can stress test these protocols under various market conditions, uncovering potential vulnerabilities before they are exploited.

.svg)

.svg)