Chainrisk Simulation Engine

Chainrisk Simulation Engine provides rapid, precise DeFi risk assessments using Rust-based simulations & on-chain data, optimizing protocols for resilience & cost-efficiency.

November 8, 2024

Value at Risk (VaR) widely adopted by both traditional and DeFi institutions to gauge potential losses within portfolios under varying market conditions. In DeFi, VaR’s relevance has grown as protocols seek robust methodologies to manage bad debt and counter extreme market volatilities.

This blog explores the core principles of VaR, its calculation methods—including historical simulation, variance-covariance, and Monte Carlo simulation—and its critical applications within financial risk management.

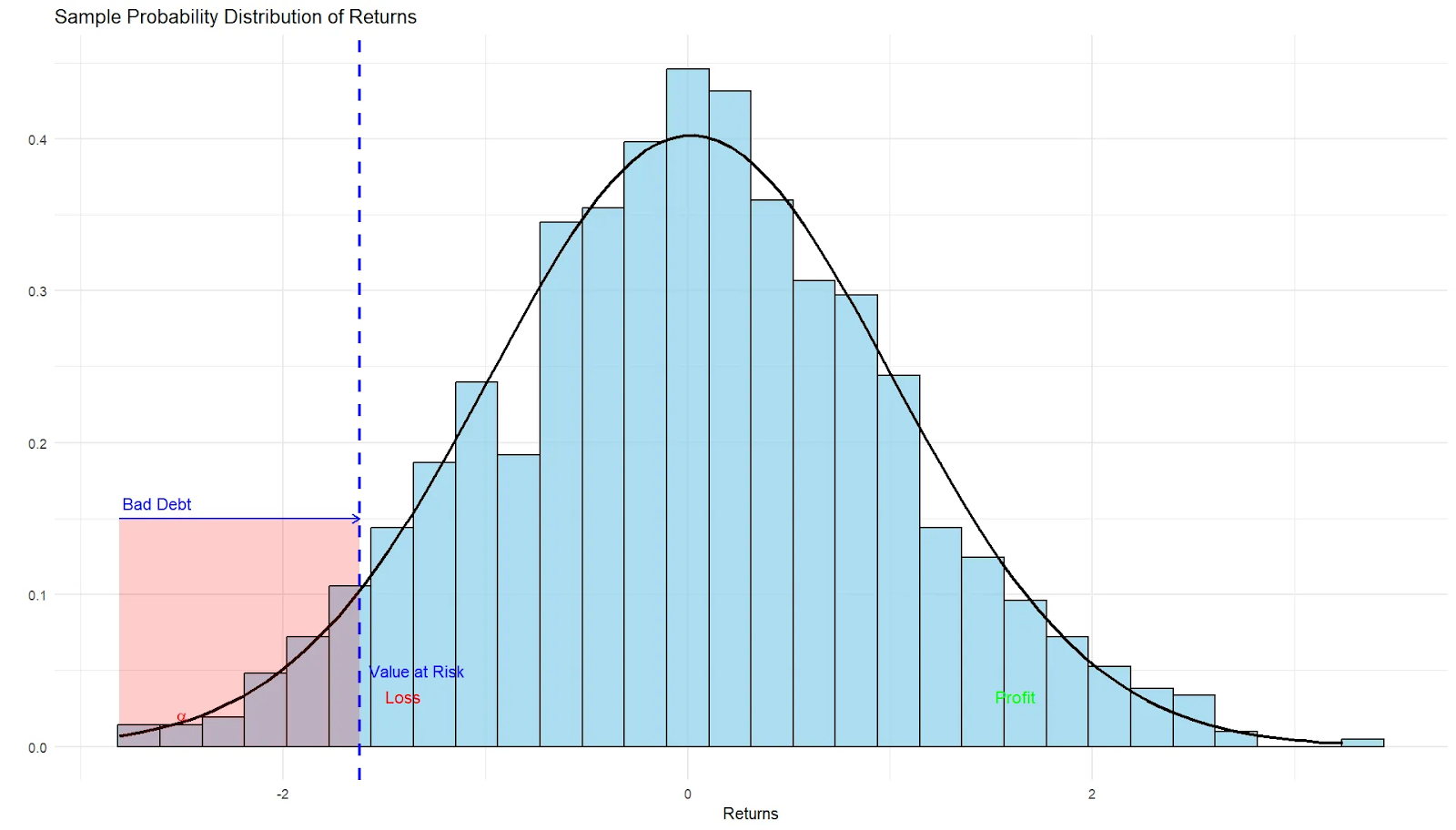

Value at Risk (VaR) is a statistical measure used in finance to quantify the level of risk within a portfolio or investment over a specific time frame. VaR, inspired from the statistical concept of variance 𝛔2 is used to capture the variance that can be present in the observed potential loss under different market conditions.

One of the use cases of VaR is to estimate the maximum potential loss with a given confidence level (usually 95% or 99%) under various market conditions. For example, a one-day VaR at the 95% confidence level of $1 million means there is a 95% probability that the institutions (or Portfolio in traditional finance) will not lose more than $1 million in one day.

VaR can be found widely in any literature of traditional financial markets. However, it is also being used extensively to understand the potential bad debt (loss) that can be incurred by Decentralized Financial (DeFi) institutions as well, like protocols and others.

In financial risk management, alpha (ɑ) is the probability of experiencing extreme losses and is directly tied to the calculation of Value at Risk (VaR). VaR is estimated at a specific confidence level, which is defined as 1-ɑ. For instance, if ɑ=0.05, this corresponds to a 95% confidence level, meaning there is a 5% chance that losses will exceed the VaR threshold within a given time period.

By selecting different values of alpha, risk managers can adjust the strictness of VaR estimates, with lower alpha values (higher confidence levels) indicating more conservative risk assessments.

This relationship between alpha and VaR allows institutions to set risk limits based on their tolerance for extreme loss scenarios. The VaR depicted in the graph corresponds to the 95th percentile of the distribution, and any loss below that point is an extreme bad debt (loss).

VaR, a statistical estimate of the spread of the DeFi institutes loss can be computed in numerous ways. Some of which are just touched upon in this section.

Start with a set of simulations (say for sake of illustration, $2000$) using an initial set of model parameters, s. These parameters have been decided upon using the historical price data.

After these simulations, calculate the 95th percentile (say Xi) of the resulting losses. This represents the loss level that has only a 5% chance of being exceeded, giving an initial bad-debt estimate.

To confirm the reliability of the 95th percentile estimate, conduct an additional set of simulations using the same model parameters, s as done earlier. Now, we recalculate the 95th percentile (say Xi+1) bad debt based on the new appended observed bad-debt values.

The two observed 95th percentile values are compared. If the difference Xi+1-Xi is within a specified tolerance level 𝝐 ,i.e., Xi+1-Xi ⩽𝝐, then Xi+1 is considered as the VaR.

If not, additional simulations are done until the difference is within the tolerance limit.

Value at Risk (VaR) plays a vital role in risk management by providing institutions with a clear measure of potential losses, allowing them to navigate market uncertainties with confidence. This section explores how VaR is applied in practical settings to maintain financial stability, support balanced growth, and prepare for extreme market conditions.

Financial institutions set specific risk limits for portfolios or trading activities based on VaR calculations, ensuring that investments remain within the organization’s risk tolerance and support capital preservation. This helps prevent excessive risk-taking by aligning daily operations with long-term financial stability goals.

Although VaR focuses on normal market conditions, pairing it with stress testing allows institutions to assess how portfolios might perform during extreme, atypical events. This combination provides a more complete risk profile, helping firms prepare for and withstand unexpected shocks.

Firms use VaR insights to proactively adjust portfolio allocations, avoiding overexposure to riskier assets. This helps align investment strategies with both market conditions and the organization’s risk appetite, enhancing resilience and promoting balanced growth.

To simulate usual market conditions, and understand the market dynamics in a more general way, we use the 95th percentile values. Also we can use a more rigorous condition of taking the 99th percentile value in place of the 95th value, which can help us to check for the extreme market conditions and check for the extreme market scenarios.

Value at Risk (VaR) is a powerful tool that helps financial institutions measure and manage potential losses, keeping risk within acceptable limits. Whether in traditional finance or DeFi, VaR’s various calculation methods—like historical simulation and Monte Carlo simulation—offer flexible ways to understand and prepare for potential downturns. As markets face constant shifts, VaR remains essential for helping organizations stay steady through uncertainty, ensuring that they’re equipped to handle unexpected challenges while keeping their financial strategies on track.

.svg)

.svg)